Board Director AI Alert: 2026 and the New Era of AI Accountability

The year 2026 will mark a major shift in how organizations are evaluated on their use of artificial intelligence. Over the past two years, many boards have focused on exploring AI’s strategic upside, targeting cost reductions, productivity gains, and new product opportunities. The next two years are likely to look very different. A new era of AI accountability is arriving, driven by three converging forces that are moving governance from a theoretical exercise to an urgent business imperative.

The Converging Forces Driving Change

A trio of powerful, interconnected pressures is propelling this fundamental shift:

Regulatory Formalization: Across the U.S., EU, U.K., Canada, and APAC, AI rules are rapidly moving from voluntary guidance to enforceable compliance obligations. The U.S. Securities and Exchange Commission (SEC) itself flagged artificial intelligence disclosures as a priority in its 2024 disclosures-review cycle.

Investor Expectations: Institutional investors and private-equity firms are beginning to ask critical questions: Where is the AI risk oversight model? Who is accountable at the board level? How are you ensuring controls, fairness, data-stewardship, and security?

Vendor and Platform Accountability: Major enterprise AI providers are preparing to require governance attestations from their customers to access higher-risk model capabilities and workflow integrations.

Boards that wait until these requirements are mandatory will face reactive compliance, rushed control frameworks, reputational exposure, and delayed innovation. In contrast, boards that prepare now will secure a distinct competitive advantage, not just compliance.

What SEC Filings Reveal: AI Risk is Now Material

Public company disclosures now include AI-specific risks at a scale and depth that signal board-level urgency. The materiality of AI risk is no longer speculative, and its disclosure is increasingly the norm.

According to a recent analysis of 10-K filings for the S&P 500, 72% of companies disclosed at least one material AI risk in 2025 — up from approx. 12% in 2023 (Harvard Law Corporate Governance Forum; The Center for Audit Quality). Further data shows that 90% of S&P 500 companies mentioned AI-related information in their 2024 Form 10-K filings (The Center for Audit Quality).

Disclosures show a heavy emphasis on cybersecurity and data-privacy risks: one study found that 2 in 5 companies cited AI-enabled cyber threats, and at least 100 filings mentioned bias in AI inputs/outputs (cslawreport.com).

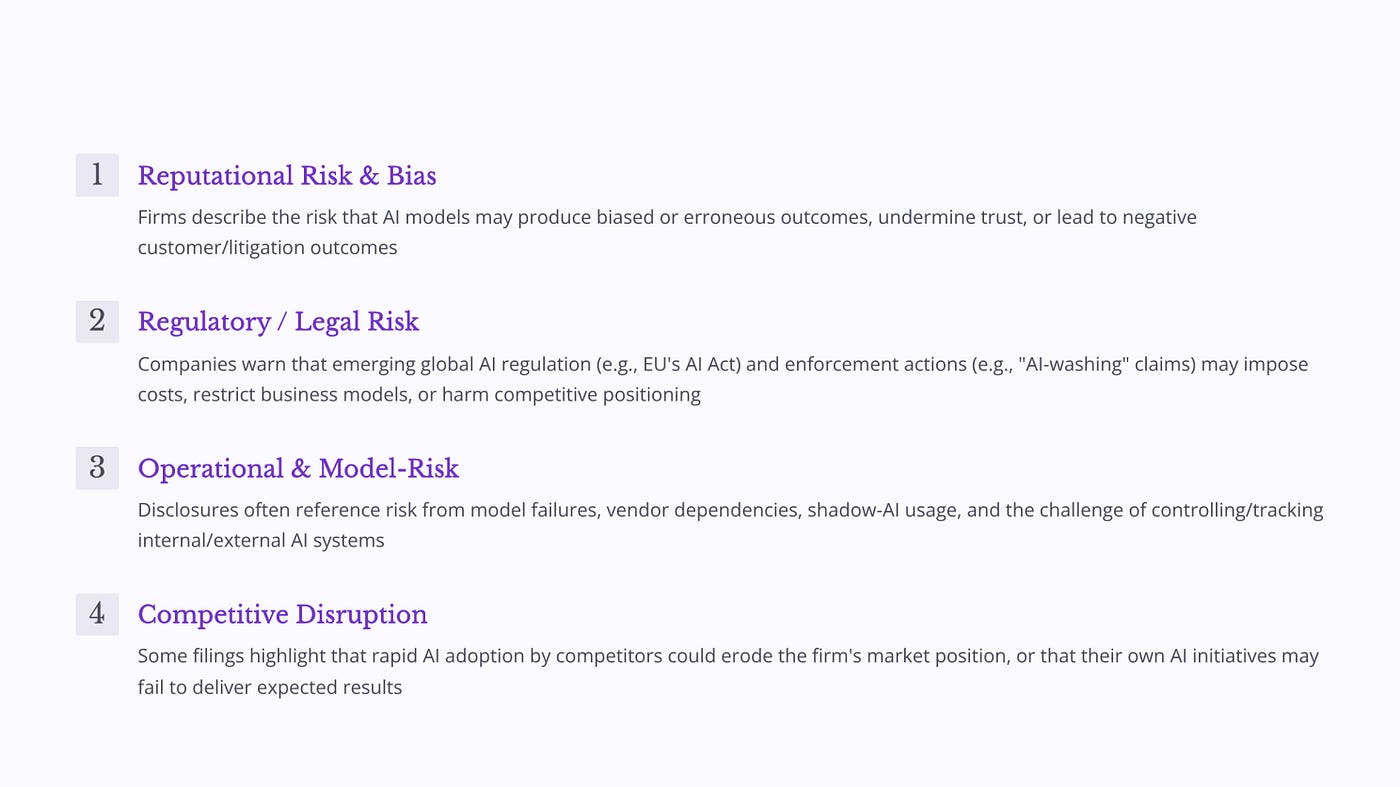

These trends highlight several key risk themes emerging in disclosures:

What companies are saying in their filings

Boardroom shifts for 2026

Given these pressures, boards must anticipate a new set of expectations. The focus is moving from high-level strategy to documented, defensible governance. These implications require new organizational capabilities:

From Awareness to Accountability

If 2024–2025 was the era of AI strategy and awareness, 2026 will be defined by AI accountability, risk management, and a rigorous focus on return on investment (ROI). Boards must assume that AI exposure is already on the investor radar and that the window for voluntary adoption of best practices is rapidly closing.

References

Bass Berry Securities Law Exchange. (2025). Navigating AI regulatory and legal risks in public disclosures.

CSLawReport. (2025). Analysis of AI-enabled cyber threats and bias in corporate filings.

Harvard Law School Forum on Corporate Governance. (2025). The growth of material AI risk in S&P 500 disclosures.

Intelligize. (2025). Cybersecurity and data-privacy: New AI vectors in corporate risk factors.

Securities and Exchange Commission. (2024). 2024 disclosures-review cycle priorities.

The Center for Audit Quality. (2024). AI in 2024 Form 10-K filings: An S&P 500 analysis.

The Center for Audit Quality. (2025). Trends in material AI risk disclosures: 2023–2025.